__PRESENT__PRESENT

__PRESENT__PRESENT__PRESENT

__PRESENT

__PRESENT

__PRESENT

Transcript: Weekly Wrap 4 April

Locally this week the RBA held the nation’s cash rate at 4.1% for the next period as Australia’s central bank waits for the potential impacts of Trump’s ‘Liberation Day’ tariffs and to ensure the current inflation journey is sustained not just a momentary dip in the CPI reading.

On the note of Trump’s latest Tariffs, let’s dive into Liberation Day, what was announced and what the impacts of such taxes will be on both Australian businesses and you as an investor.

April the 2nd was Trump’s Liberation Day whereby he handed down a new array of tariffs on countries he believes has been unfairly taxing US imports for some time, and Australia was not exempt from the taxes this round. The key word of his speech was reciprocal, which he repeated over and over to ensure countries he imposed the new taxes on would understand the tariffs are due to taxes they imposed on US exports in recent times. As he stood at the podium holding a chart of countries tariffs on the US and the newly imposed reciprocal tariffs on those countries, the world braced for what this may mean for global trade.

Firstly, the President announced a baseline 10% tariff on imports from all countries that trade with the US except those that comply with the USMCA free trade agreement, with Vietnam, Sri Lanka, Madagascar and Cambodia the hardest hit in Trump’s tariff announcements as the US president handed down a 46%, 44%, 47% and 49% reciprocal tariff respectively on each of these countries. Of the larger nations, the reciprocal tariffs imposed are as follows: Australia 10%, China 34% totalling 54% after initial 20% announced a while ago, European Union 20%, Taiwan 32%, Japan 24%, India 26%, South Korea 25%, Thailand 36%, Japan 24%, Israel 17% and India 26%, with each of the tariffs announced going into effect from April 5.

South Korea and Japan are expected to bear much of the brunt of Trump’s newly introduced 25% automotive tariff with these regions ranking 2nd and 3rd among the countries with the highest automotive trade with the US, but the effects of the newly announced automotive tariff will be felt far and wide.

Aussie beef imports were a notable feature of Trump’s Liberation Day speech. The US president outlined that Australia’s ban of US beef comes after the US imported $3bn of Aussie beef in 2024 alone. Mind you, Australia has had the ban on importing US beef since 2003 following the outbreak of mad cow disease in the US. President Trump said as a result of Australia banning US beef exports, he would impose the same on importing fresh Aussie beef, of which the US is Australia’s largest red meat market so this will likely hurt our national beef industry. Trump also ruled out any exemptions unless countries agreed to terminate their tariffs on the US, to which PM Albanese said we will not compromise biosecurity. While Trump said he will ‘do the same’ to Australian beef, we are yet to know the full extent of his tariff on Aussie beef so watch this space. If he does ban Aussie beef we will likely see a rise in the price of beef locally as the farmers may reduce the cattle production to ensure financial viability is maintained.

While the President’s intentions are to enhance US domestic demand and production, and support Americans with tax cuts, the opposite effect is bound to happen. Companies that now face a 10% tariff on any goods going to the US will inherently pass on the tax to the end user, the American people, by hiking prices to accommodate for the higher cost to send products to the US. We may also see more M&A activity to get around the tariffs which we have already seen through James Hardie’s move to acquire AZEK in the US to ensure products are made on US soil thus are exempt from the US tariff.

Australia’s Prime Minister Anthony Albanese said Australia will not impose reciprocal tariffs back on the US, but the act of Liberation Day is not the act of a friend.

With the tariffs now announced, what will this mean for you as an investor. Any of the equities you hold that have exposure to the US through supplying goods to the region will now face the 10% blanket tariff imposed on Australian goods being exported to the US. This doesn’t necessarily mean hit the sell button, but it is important that you analyse how the company responds to the tariff, if they implement price hikes and to what degree they will pass on the cost. If they do increase prices to the US, that is a good thing as the tariff won’t impact their bottom line.

The high volatility and global uncertainty at the moment has fuelled further demand for gold exposure in investors’ portfolios which propelled the price of the precious commodity to a fresh record US$3148.96/ounce this week.

The tariff outlay will likely have an impact on global trade, global economic growth and global economic stability but there is no reason for panic selling, instead, digest the information and remember your investment strategy.

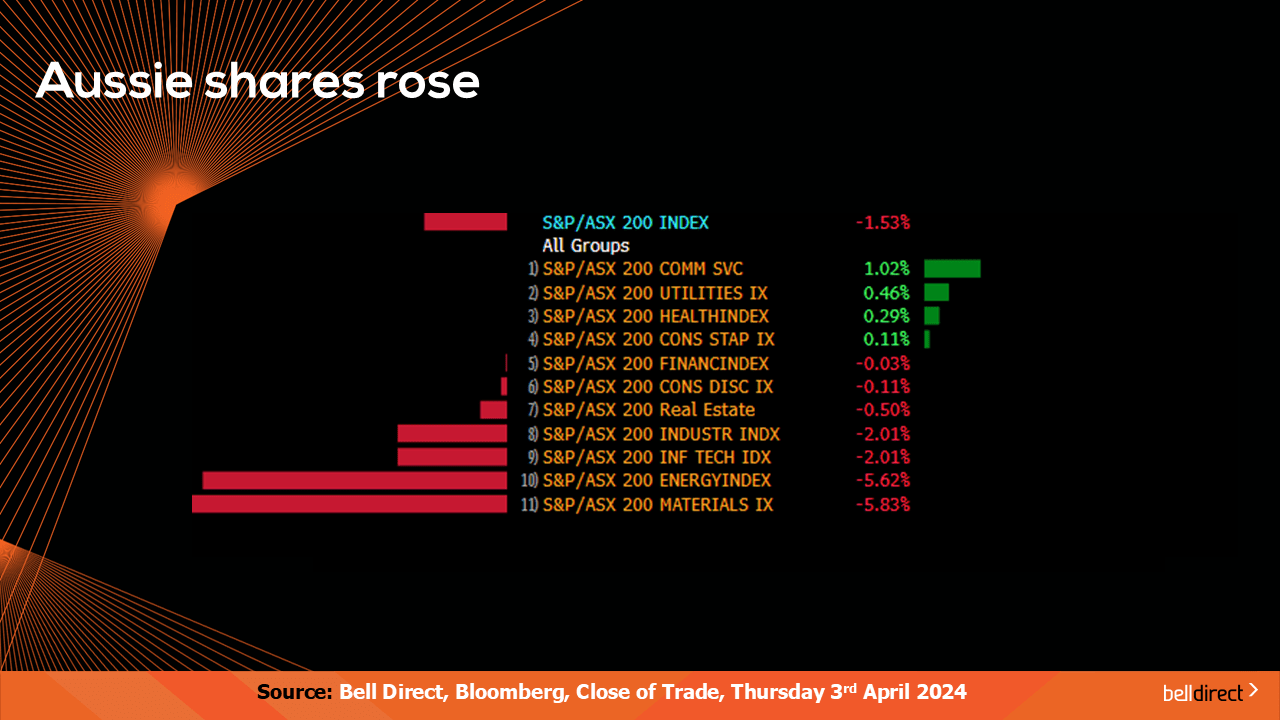

Locally from Monday to Thursday, the ASX200 tumbled 1.53% as global market uncertainty spilled into the local market and weighed on investor sentiment. Materials and energy stocks took the biggest hit with these sectors posting declines of 5.83% and 5.62% respectively as investors are concerned over the impact of Trump’s tariffs on such sectors.

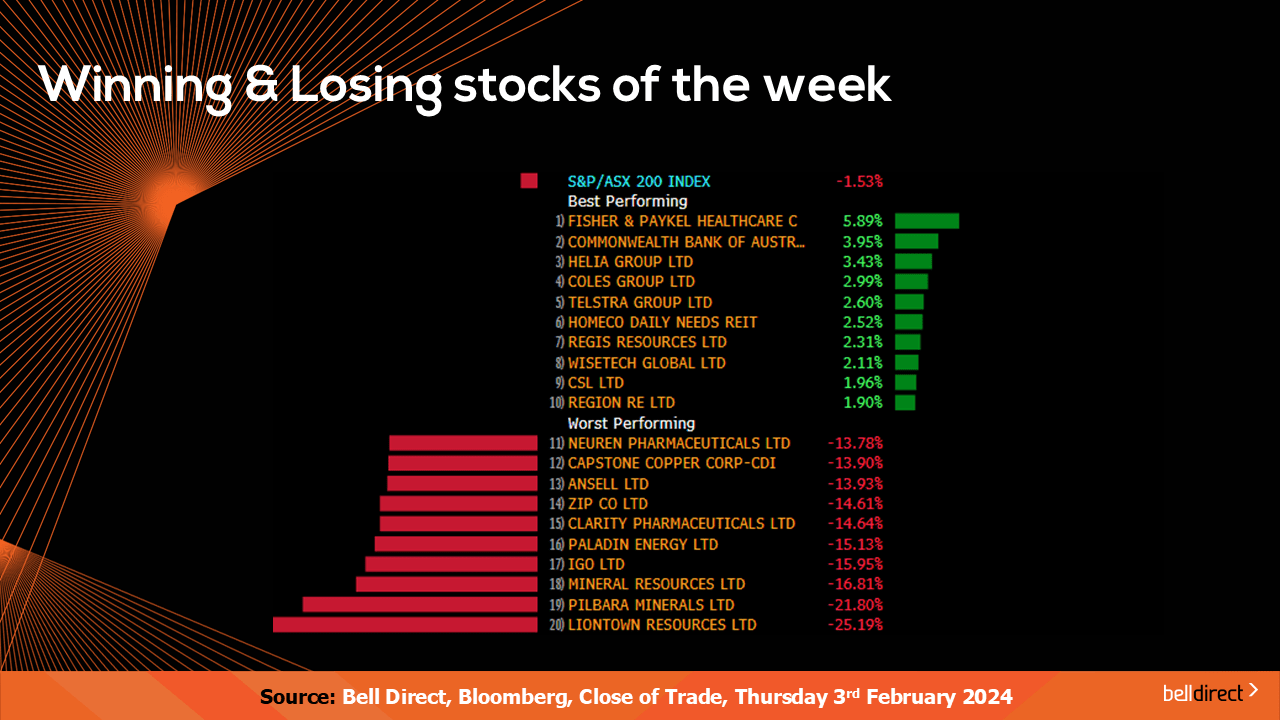

The winning stocks on the ASX200 this week were led by Fisher and Paykel (ASX:FPH) rising 5.9%, CBA (ASX:CBA) adding almost 4% and Helia Group (ASX:HLI) rallying 3.43%. On the losing end Liontown resources (ASX:LTR) tanked over 25%, PLS (ASX:PLS) fell 21.8% and Mineral Resources (ASX:MIN) ended the week down a further 16.81%.

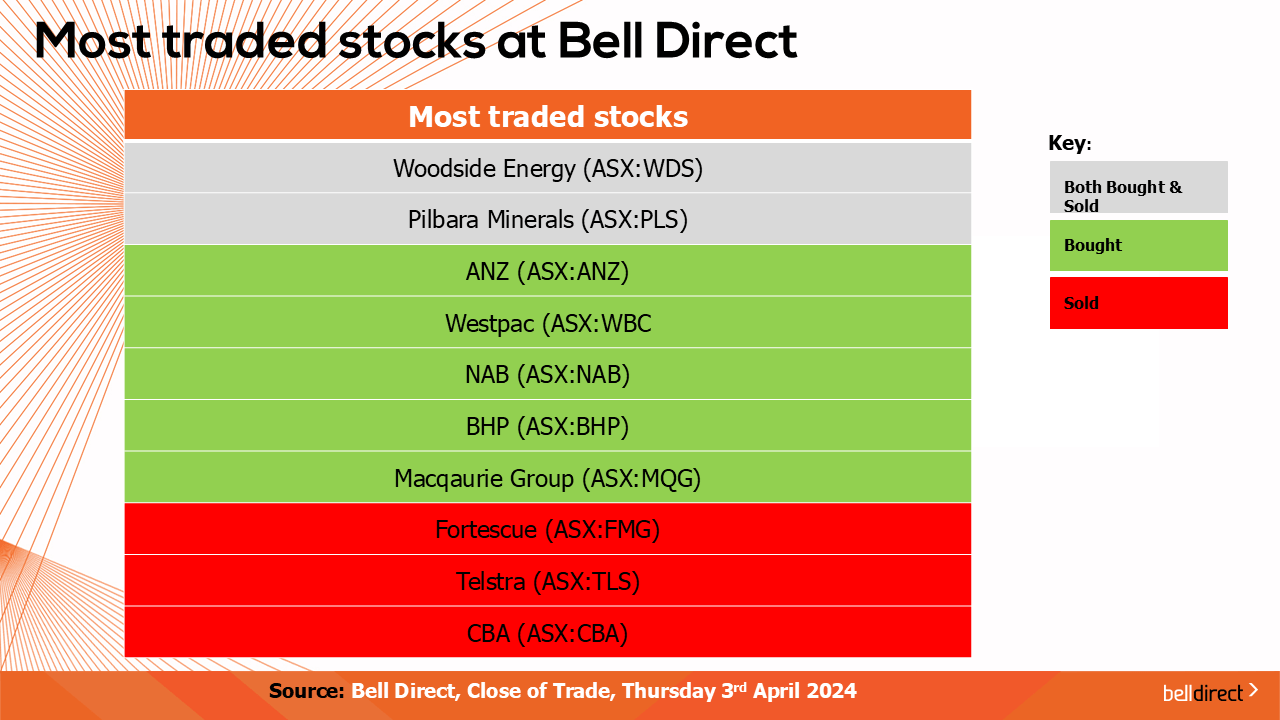

The most traded stocks by Bell Direct clients this week were Woodside (ASX:WDS), PLS (ASX:PLS), ANZ (ASX:ANZ), Westpac (ASX:WBC) and NAB (ASX:NAB).

Clients also bought into BHP (ASX:BHP), Macquarie Group (ASX:MGQ), and Fortescue (ASX:FMG), while taking profits from Telstra (ASX:TLS) and CBA (ASX:CBA).

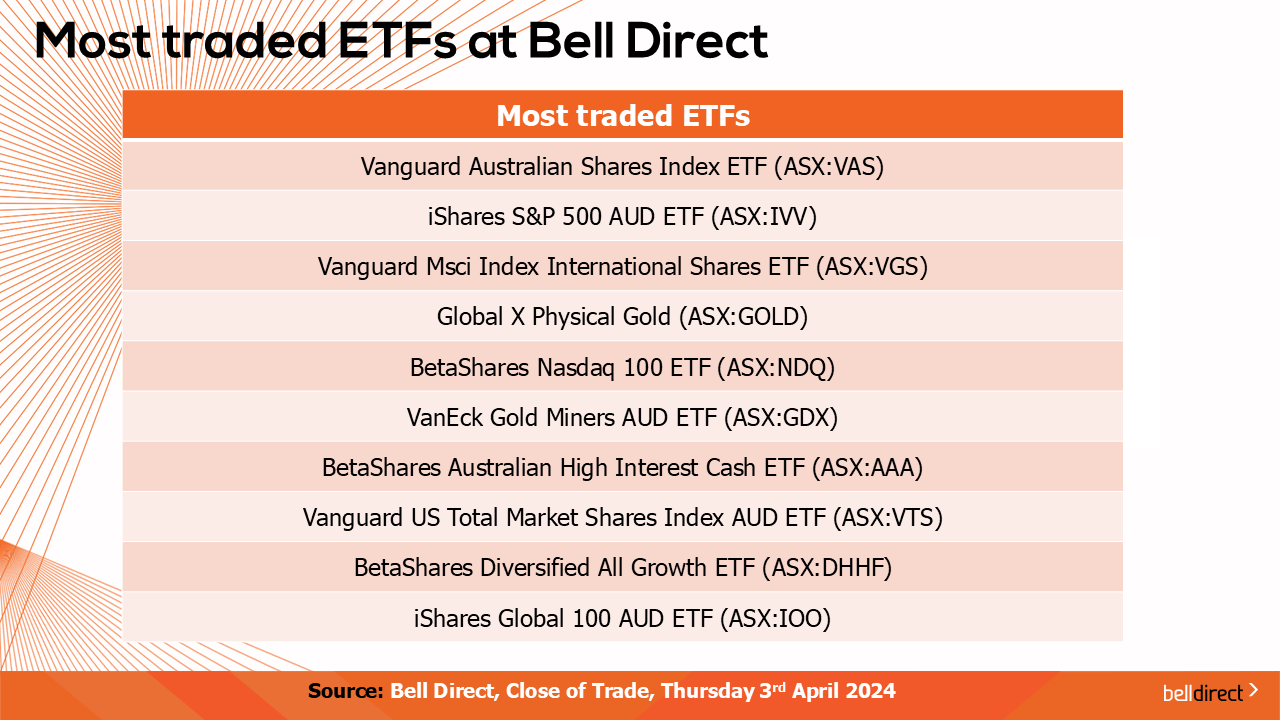

And the most traded ETFs were led by Vanguard Australian Shares Index ETF, iShares S&P 500 AUD ETF and Vanguard Msci Index International Shares ETF.

On the economic calendar next week, we may see local investors respond to Westpac Consumer Confidence data for April and NAB Business Confidence data for March both out on Tuesday with the forecast of a decline in both consumer and business confidence amid the unfolding global trade war.

Overseas, it is a big week for the US with the FOMC meeting minutes, core and headline inflation readings and producer price index data out in the US, while in China, trade balance data is out later in the week.

And that’s all for this Friday, have a fantastic weekend and happy investing.